Multigenerational Living in the Age of High Housing Costs: Why Twin Falls Families Are Turning to ADUs

TL;DR:

Idaho's median home price has climbed past $475,000 statewide. In Twin Falls, the median sits around $335,000 to $363,000, with a median household income of roughly $61,000 to $68,000. That math doesn't work for a lot of families. Multigenerational living is surging nationally (14 to 17% of all home purchases in recent years), and ADUs are the tool that makes it practical without sacrificing anyone's privacy. Whether you're housing an aging parent, an adult child saving for their first home, or a family member in transition, an ADU keeps housing costs within the family while building equity on property you already own. This guide covers why it's happening, who it works for, and how to set it up without damaging the relationships that make it worth doing.

There's a quiet shift happening in neighborhoods across the Magic Valley. Families who would have spread out across separate homes a generation ago are choosing to stay closer together, not because they want to, but because the economics of housing have made separation increasingly unaffordable.

This isn't a cultural trend story. It's a math story. And the math is pushing more Twin Falls families toward a solution that was once considered unconventional but now looks like the most practical option available: building an ADU in the backyard and keeping the family on one property.

The Numbers That Are Driving This Shift

Idaho's housing market has changed fundamentally over the past five years, and it's not going back.

Statewide, the median home price has surged past $475,000. That represents a roughly 50% increase from pre-pandemic levels. According to Redfin's March 2026 data, the median sale price in Idaho was $476,300, and while that's down slightly year-over-year, it remains far beyond what most Idaho families can comfortably afford.

In Twin Falls, the picture is more moderate but still challenging. The median home price sits around $335,000 to $363,000, depending on the data source, with a median household income of approximately $61,000 to $68,000. At current mortgage rates (mid to high 6% range), a $335,000 home with 20% down produces a monthly payment of roughly $1,800 to $2,000 including taxes and insurance. That's 35 to 40% of a median-income household's gross pay, well above the 30% threshold that defines affordable housing.

For younger adults, the barrier is even steeper. A starter home in Twin Falls averages $278,000, requiring roughly $56,000 in down payment and closing costs. For a 28-year-old earning $40,000, that's more than a year's gross income just to get in the door. And statewide, only 17% of homes listed for sale are affordable to households earning $100,000.

For older adults, the squeeze works differently. A parent on a fixed income of $2,500 per month (typical for Social Security plus a modest pension) can't afford $1,100 in rent plus utilities, food, transportation, and healthcare. But they may not need or want the full infrastructure of assisted living, which runs $3,800 to $5,200 per month in Idaho. They need an affordable, independent living situation near family. That's precisely what an ADU provides.

Multigenerational Living Is No Longer the Exception

This isn't a fringe arrangement. The National Association of Realtors reports that 17% of all homes purchased in 2024 were for multigenerational households, a record high. The 2025 report showed a slight dip to 14%, but the trend line over the past decade points clearly upward.

The reasons are consistent: cost savings, caregiving for aging parents, and adult children who can't afford to buy on their own. In Idaho specifically, Zillow's 2025 Zeitgeist report flagged the state as a leader in searches for ADUs, guest houses, casitas, and in-law suites, all terms that signal multigenerational intent.

What's changed isn't the desire. Families have always wanted to stay close. What's changed is that the traditional alternative (everyone buys their own house) has become financially impossible for a growing share of the population. An ADU on property you already own is the most cost-effective way to add housing capacity for your family without entering a market that's priced against you.

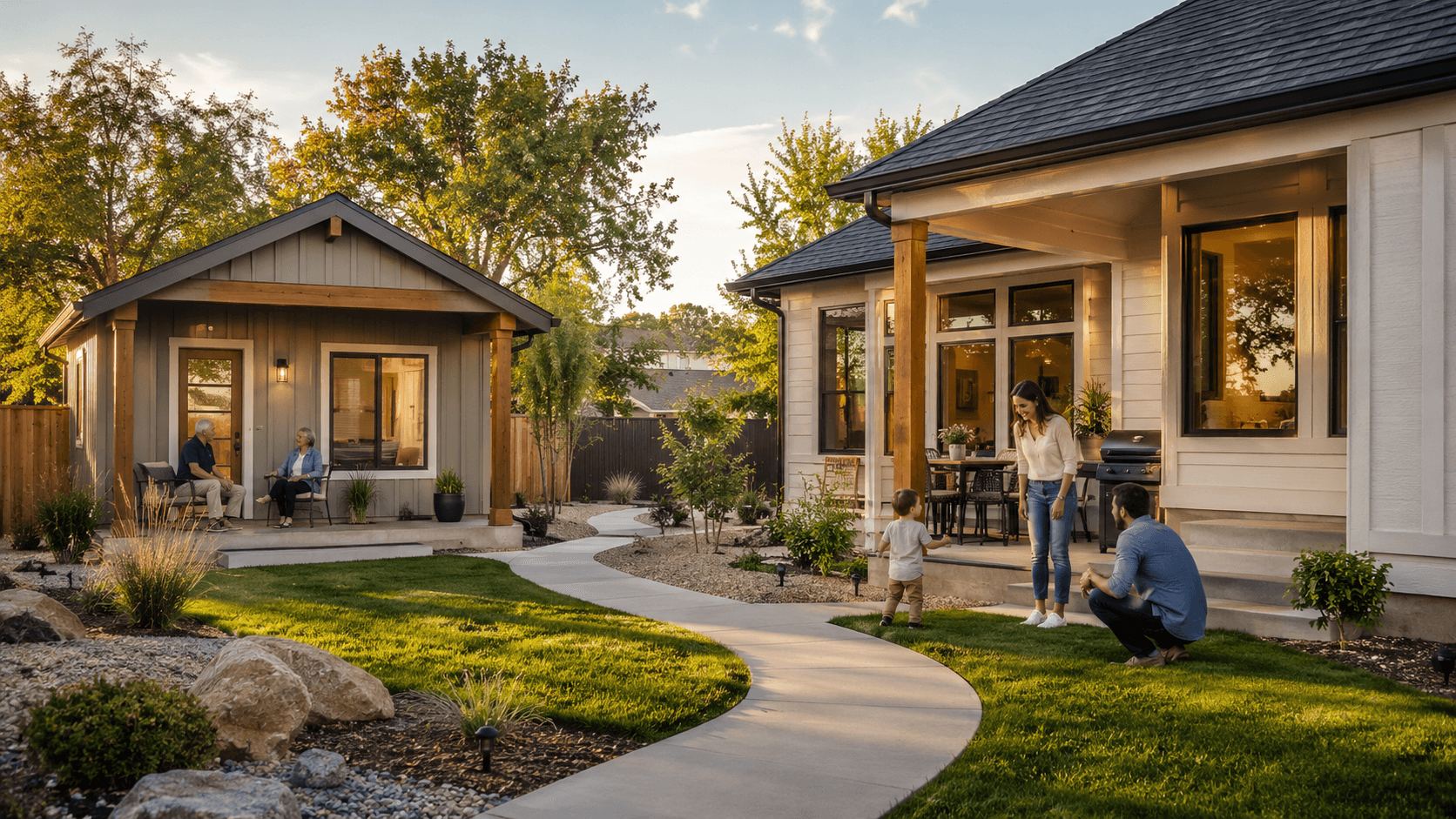

Three Families, Three ADU Scenarios

Multigenerational ADU arrangements aren't one-size-fits-all. The design, the financial structure, and the boundaries look different depending on who's moving in and why.

The aging parent

The situation: Your mother is 74, healthy, and independent. She lives alone in a three-bedroom house an hour away. You worry about her, she's lonely, and her home maintenance costs are eating into her fixed income.

The ADU solution: A 550 sq ft detached unit with zero-step entry, curbless shower, wide doorways, and wall blocking for future grab bars. She sells her house (freeing up equity), moves into the ADU, and lives independently with family support next door. Her housing cost drops to whatever utility contribution you agree on, instead of $1,500 per month in mortgage, taxes, insurance, and maintenance on a house she no longer needs.

The financial math: Building the ADU costs $120,000 to $150,000. Assisted living would cost $42,000 to $62,000 per year. The ADU pays for itself in two to four years, and it remains a valuable asset (rentable at $900 to $1,100/month) when she no longer needs it.

For a deeper dive into aging-in-place design features, accessibility standards, and the full financial comparison to assisted living, see our guide to building an ADU for aging parents.

The adult child saving for a home

The situation: Your 26-year-old son works full-time, earns $42,000 a year, and is drowning in rent. He's been trying to save for a down payment, but paying $1,100 per month for an apartment in Twin Falls leaves almost nothing for savings. At this rate, it'll take him five to seven years to accumulate a starter home down payment.

The ADU solution: He moves into the ADU at fair market rent ($900 to $1,000 per month), which saves him $100 to $200 per month compared to his apartment. More importantly, his rent now stays within the family. You use the rental income to pay down the ADU's construction loan. He gets stable, affordable housing close to family. You get a tenant you trust. And in two to three years, he's saved enough for a down payment on his own place.

The financial math: At $200 per month in savings versus his apartment, he accumulates $7,200 over three years just from the rent difference. If you also set aside a portion of his rent payments as an informal family savings match, the timeline to homeownership accelerates further.

The family member in transition

The situation: Your sister is going through a divorce. She has two kids, a part-time job, and needs a stable place to land while she figures out her next step. Apartments require first/last/deposit ($3,000 to $4,000 upfront), credit checks she's worried about, and 12-month leases that don't match her timeline.

The ADU solution: She moves into the ADU under a month-to-month lease at a modest family discount. The kids have a yard, proximity to cousins, and stability during a chaotic time. She has privacy and independence without the financial pressure of market-rate housing during a vulnerable period.

The practical consideration: Transition arrangements are the most emotionally charged and the most important to formalize with a written agreement. A clear timeline, monthly check-ins, and defined expectations prevent a temporary stay from becoming an indefinite one.

For the tax implications, lease essentials, and boundary-setting guidance that apply to all three scenarios, see our guide to renting your ADU to a family member.

Why an ADU Beats Every Other Option

Multigenerational families have always found ways to live together. What makes an ADU different from the traditional approaches is that it solves the problem without creating new ones.

Compared to moving in together (shared house): An ADU gives each household a separate entrance, separate kitchen, and separate daily routine. The proximity is there, but the independence is preserved. Sharing a house with adult family members works for some families, but for most, the loss of privacy creates friction that builds over months and years. An ADU eliminates that pressure entirely.

Compared to renting a nearby apartment: An ADU keeps housing costs within the family. Rent paid to a landlord builds someone else's equity. Rent paid on a family ADU either covers your construction loan or goes into your pocket. And the unit itself adds value to your property. An apartment adds value to nothing.

Compared to buying a second property: As we covered in our ADU vs. rental property comparison, building an ADU on land you already own produces a higher cash-on-cash return than purchasing a separate property at current Twin Falls prices. You skip the down payment, closing costs, and second mortgage entirely.

Compared to assisted living (for aging parents): An ADU costs $120,000 to $175,000 once. Assisted living costs $42,000 to $62,000 per year in Idaho, every year, with annual increases of 3 to 7%. The ADU pays for itself in two to four years and remains a family asset indefinitely.

Idaho's 2026 Laws Make This Easier Than Ever

The timing for multigenerational ADU projects in Twin Falls has never been better from a regulatory standpoint.

Senate Bill 1354, signed into law on March 31, 2026 and effective July 1, requires all Idaho cities with populations over 10,000 to allow at least one ADU per single-family lot. Owner-occupancy requirements are eliminated. Size caps cannot be set below 1,000 sq ft or 75% of the primary home. Parking requirements are removed in most cases.

House Bill 800 creates a new administrative path for lot splits on properties with ADUs, enabling separate ownership or financing of the ADU portion. This could eventually allow a family member to own the ADU independently.

Our full breakdown of Idaho's 2026 housing bills explains every provision and what it means specifically for Twin Falls homeowners.

The Conversation Nobody Wants to Have (But Everyone Should)

The hardest part of multigenerational ADU living isn't the construction, the permitting, or the financing. It's the family conversation that precedes all of it.

Before anyone moves in, the family should agree on:

How long the arrangement is expected to last (even a rough timeline helps). What rent will be charged, if any, and how utilities will be handled. How shared outdoor space (yard, driveway, patio) will be used. What the communication norms will be (knock first, text first, open door policy). What happens when the arrangement ends, and how much notice each party gives.

These aren't fun conversations. They feel overly formal for family. But every experienced ADU homeowner will tell you the same thing: the families that talk about boundaries before move-in are the ones still talking to each other after.

Frequently Asked Questions

Is multigenerational living really more affordable than everyone having their own place?

In most cases, significantly so. A family with an aging parent in the ADU saves $42,000 to $62,000 per year compared to assisted living. An adult child paying $900 in ADU rent instead of $1,100 for an apartment saves $2,400 per year, and that rent stays in the family rather than going to a landlord. The ADU itself adds property value that benefits the homeowner for decades.

What if my family member can't afford to pay rent?

That's a personal decision, not a legal one. You can let a family member live rent-free. However, you'll lose rental expense deductions on your taxes (depreciation, maintenance, insurance). For aging parents on fixed incomes, many families absorb the cost as an alternative to assisted living. The savings still overwhelmingly favor the ADU.

Does my property need to be a certain size?

Under SB 1354, cities cannot require minimum lot sizes larger than what's required for a single-family home. Your lot still needs enough room for setbacks, parking, and adequate utility access. A feasibility check is the fastest way to find out what your specific property can support.

Can I build an ADU even if I have an HOA?

Under SB 1354, HOAs cannot add new restrictions on ADUs after the law takes effect. However, if your CC&Rs already prohibited ADUs when you purchased, that restriction may still be enforceable. Review your HOA documents carefully.

What if the family member eventually moves out?

The unit becomes a market-rate rental generating $900 to $1,100 per month in Twin Falls, a guest house, a home office, or a selling point that increases your resale value. An ADU built for family use today is a flexible asset for whatever comes next.

How do I get started?

A feasibility check on your property is the first step. It tells you what you can build, what it will cost, and what constraints (zoning, utilities, lot coverage) you'll be working with. Everything else follows from that data.

Housing costs aren't coming back down. Families who wait for affordability to "return to normal" may be waiting a very long time. An ADU on property you already own is a way to take control of the situation right now, for the generation that needs help today and the one that will need it tomorrow. Reach out to Twin Falls ADU Guys for a feasibility check, and let's figure out what your property can do for your family.

Twin Falls ADU Guys Team

Twin Falls ADU Guys